Tuesday, December 23, 2025

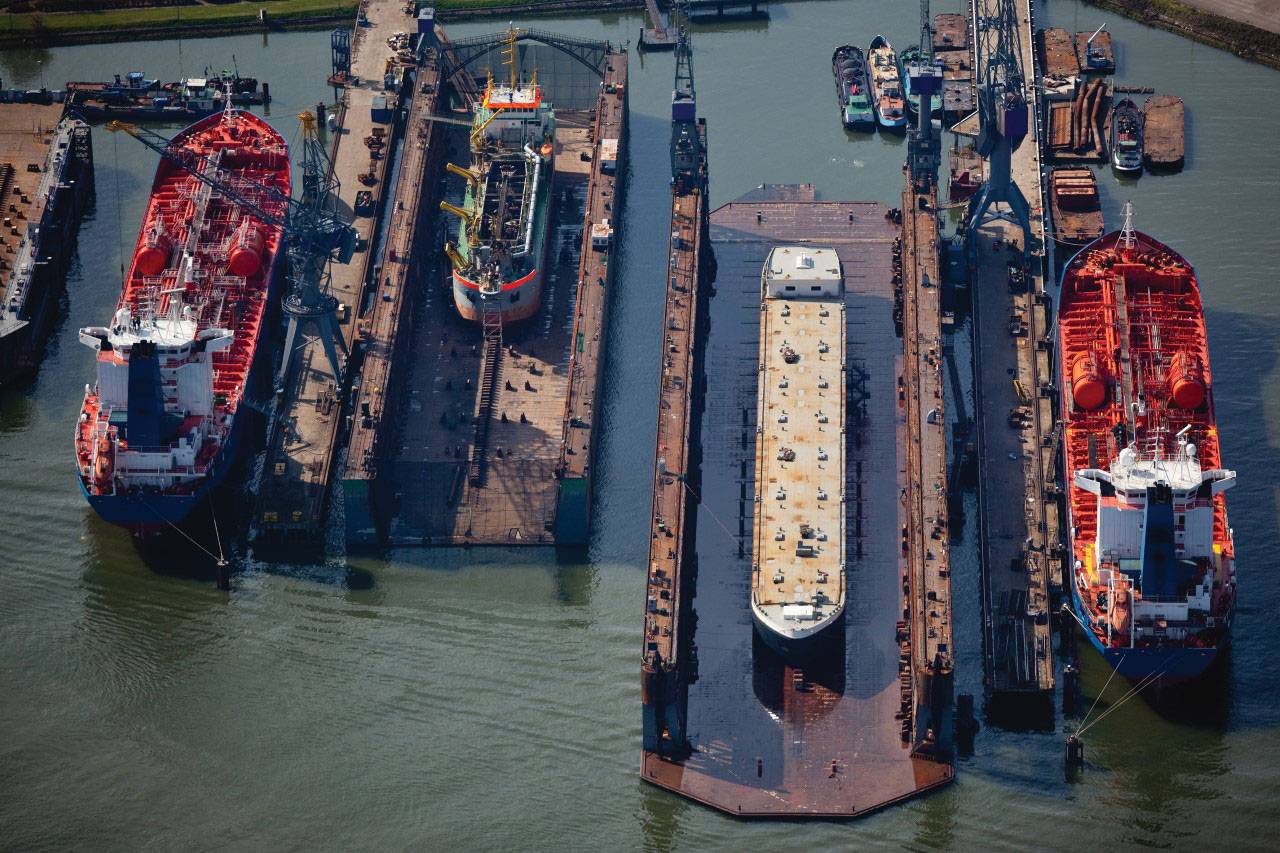

By operating on both land and water, marine repairers and equipment installers tackle a variety of tasks from general maintenance and repair, to upgrading and installing state-of-the-art systems and equipment. Along with these tasks comes a wide array of maritime risk exposures, both large and small, which the business owner needs to adequately address.

By operating on both land and water, marine repairers and equipment installers tackle a variety of tasks from general maintenance and repair, to upgrading and installing state-of-the-art systems and equipment. Along with these tasks comes a wide array of maritime risk exposures, both large and small, which the business owner needs to adequately address.

The tasks of a marine repair technician are challenging enough on their own, but try to do this work on a vessel at sea or in a shipyard, and the technician will find that the hazard level rises dramatically — from making sure that all facets of the systems work together as they should, to the increased fire risk hot work and welding presents to the safety of the vessel. As a result, only professional installers with an experienced maritime background should be considered for such work. Vessel owners and shipyards should be sure to contract only with ship repairers and installers who have comprehensive insurance that will not only protect that but also provide coverage for the vessel or shipyard if the installer is found responsible for any damage. This would be done by ensuring the repairer or installer has proper and adequate insurance along with written contractual risk transfer. The exposure for vessels in their care, custody, and control, along with any other potential third-party property damage must be addressed.

While most maritime repairers and installers recognize and address these exposures, good coverage is not always easy to find for potential high hazard businesses like these. Some insurers shy away from underwriting these businesses due to the potential high-risk nature of their work. Others may be willing to insure these maritime service companies, but may not have the marine expertise to understand, address, and provide coverage for some of the “hidden” exposures of the business. By understanding how underwriters assess risk, and by implementing proper risk control measures, marine businesses will have more options when it comes to choosing an insurer that has the expertise to uncover the hidden exposures threatening their business.

An insurer with extensive ocean marine experience will closely examine risk exposures facing the business and place particular emphasis on five key criteria:

Some companies may choose not to insure repair businesses that undertake welding jobs because the “hot” work carries too much fire risk, or the technical repairs and installation of critical systems on a vessel may present a great amount of third party property damage exposure. When assessing the work performed, underwriters will examine a number of factors, including operational procedures, potential for third party damages, how they document their work, and what safety programs they employ.

On shore, marine repairers and installers may have to be concerned not only with the vessel on which they are but also with any surrounding property that could present third party liability exposures. In water, underwriters will look at where on the vessel the work is being performed — whether it is a control room, high atop the vessel, or underwater beneath the vessel — and assess the risk there along with the potential risk of damaging any adjacent vessels or property.

Experience should always be a critical factor in hiring someone for any job, and the same holds true when it comes to marine repair and installation businesses. Underwriters will consider whether the technicians are skilled and knowledgeable and what level of experience they have on similar projects. While proper training is key for a good ship repairer, often the time spent on the job can build his or her level of expertise and reduce his likelihood of an accident. The experience will be verified by underwriters reviewing past insurance loss history. While having losses may not paint a total adverse picture to the underwriter due to the fortuitous circumstances in any business, the details of the losses will be a good barometer in determining a comfort level of experience. Considerable experience in more hazardous marine repair work like welding or heavy engine or system repair may lead an underwriter to consider writing a policy for a high-risk business that otherwise may have been declined.

When working on someone else’s vessel, a contract must be involved. Underwriters will look at not only whether a contract is in place to manage third party exposures, but how and to whom the repair business executes that contract, how they communicate that contract to all parties involved, and how they incorporate changes to each project into the contract. Evidence of proper contractual risk transfer will be closely evaluated. Determining insurance requirements and proper contractual risk transfer should be addressed prior to signing any contract and performing any work. Once a contract is signed, it may be difficult to change. The person signing on behalf of the repairer or installer should be competent to thoroughly review the contract and make the decision to sign it. Finally, insurers will look to cover contractual obligations that pertain only to the operations of their Insured.

The installation of a piece of equipment a ship repairer or installer did not manufacture carries its own set of risks. There is a large potential for vicarious liability on behalf of the repairer or installer even though they did not manufacture the product. If a ship repairer were to install a new radar device — manufactured elsewhere — on a vessel, and that device shorts out and causes damage to the vessel, the installer could be held liable. They are involved in the process that potentially caused the loss. An experienced marine underwriter will examine this risk exposure, verify the ship repairer has the proper controls in place, and determine what, if any, liability they are exposed to on behalf of the manufacturer. Repairers and installers should review and address any of this potential liability before arranging an agreement with any manufacturer.

Marine underwriters understand the nature of risk within the ship repair business. The ship repairer that demonstrates higher quality operations combined with sound risk control practices and procedures can differentiate themselves from other similar ship repairers. A few key areas that can help manage ship repairer are the following:

Risk Transfer. Several key risk transfer tools Certificates of Insurance, Hold Harmless Agreements and Vendor’s Coverage by endorsement. Ship repairers vary greatly with respect how much they rely third parties, therefore, it is important for each business to carefully review and understand the extent of exposure created by every third party relationship and create effective means to control these. Your risk management team, insurance broker and legal counsel familiar with contracts and product liability law, should be part of the review team to identify exposure as well as developing appropriate control techniques for the business.

Fire Protection. Fire can be a significant exposure for the ship repairer. If proper controls are not in place, fire losses can be the most destructive exposure faced by ship repairers; not only endangering lives and destroying but also negatively impacting the repairer’s reputation. Having proper fire control equipment available, adequate automated suppression systems, when possible, combined with effective and regular training in fire safety can help to reduce the likelihood and severity of loss from fire.

Product/Vessel Modifications. In ship repair operations adding or modifying large pieces of equipment or changing the vessel’s structures can be a routine occurrence. Modifications to vessel equipment, or making structural changes that deviate from its original design that result in bodily injury or property damage could create significant liability for the repairer. It is important that repairers carefully review manufacturers’ specifications and research any special requirements that may pertain to marine installations. Additionally, if structural changes are part of any repair work, appropriate consultation with qualified marine engineers and/or naval architects may also be helpful. The job specifications and details of all work performed, possibly including photos, should be documented.

When looking for a marine insurer, the insurance agent should understand the ocean marine needs of their client, review and address their exposures thoroughly, and work with carriers who have extensive experience in developing proper coverage and risk management solutions for ocean marine policyholders. It is key to find an insurer with expertise in managing third party risk exposure, coordinating both marine and on-shore coverage, and using risk control and claim teams that specialize in ocean marine. Finding the right insurer can mean added protection — and less risk — for ship repairers, enabling them to focus on their business and their customers’ needs.

There are numerous factors that are driving global environmental regulatory growth and the growth in renewable lubricant technologies, such as natural resource constraints, standardizing requirements due to globalization, public opinion and pressure, increase in climate change concerns, new technologies, new evidence from research and overall growing Environmental Health and Safety (EHS) concerns, and most recently the improvements in the durability of lubricants made from renewable technologies. According to environmental consultants and advisors, there are currently thousands of new environmental regulations awaiting attention from legislators and regulators around the globe. Different standards hamper growth and thus, pressure to harmonize regulations is likely to continue alongside the regional and global integration of markets.

Anything can happen on a jobsite. Your equipment could malfunction or the weather might cause a whirlwind of unexpected issues, or even worse, someone could get hurt. Unfortunately, not much can be done when circumstances such as those arise, which is why developing preventive strategies is crucial to having a successful and safe project. One of those strategies is always choosing safe and reliable lifting equipment. But the question that remains: is it safer to rent or to buy?

Daily news & analysis delivered direct to your email from the world’s largest audited

circulation maritime industry publication serving the global maritime market since 1939.

Daily news & analysis delivered direct to your email from the world’s largest audited

circulation maritime industry publication serving the global maritime market since 1939.